Big GST Reform: 12% Tax Slab to Be Removed – What It Means for You

GST was implemented for the first time in 2017. Since then, it has been Changed many times. There is a lot of confusion about which item should be kept in which slab. But the changes till now were not that big. Let me tell you that now a big change is going to happen in GST and the Prime Minister has given the green signal. Now the 12% tax will be removed.

Now the thing to think about here is that :

- The 12% tax will be removed?

- What will happen to the goods that were there now?

- Will the tax on those goods be abolished? Or

- Will they be shifted and kept in another slab?

Let’s know what exactly is happening? This change is a major change after the implementation of GST in 2017, in which the 12% slab has to be shift in other slabs And the important thing is that the Prime Minister’s Office has given the In principal Approval for the removal of This GST slab Point. Probably after the Monsoon Session of the Parliament, the proposal will go to the GST Council and a decision will be taken there.

What Exactly Is GST ?

GST stands for Goods and Services Tax. It’s a comprehensive, indirect tax levied on the supply of goods and services in India. GST replaced many existing taxes, aiming to simplify the tax structure, reduce tax evasion, and promote economic growth.

Key features:

- Unified tax rate across India

- Applies to most goods and services

- Input tax credit available

- Reduces cascading effect of taxes

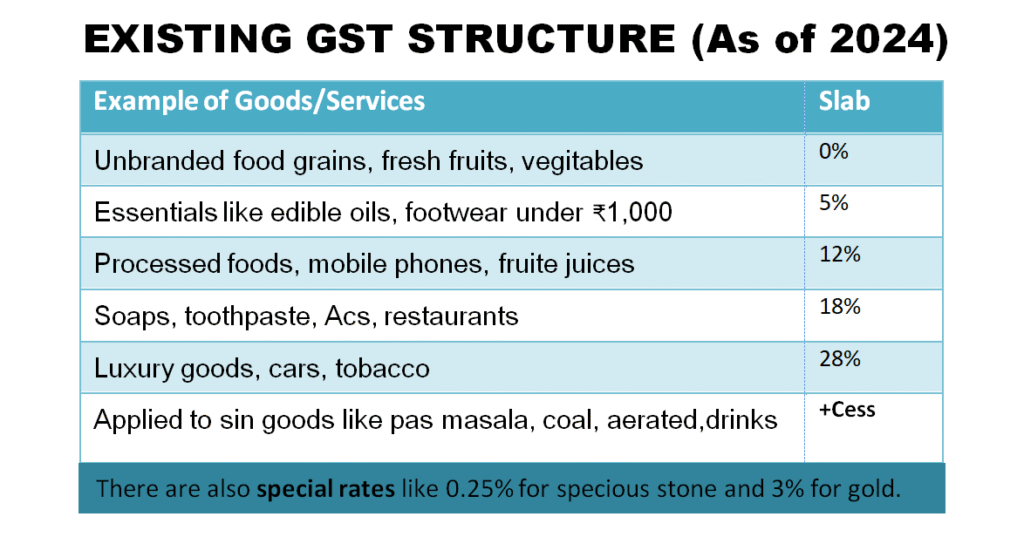

GST has various slabs (0%, 5%, 12%, 18%, 28%) for different goods and services.

Existing GST Structure

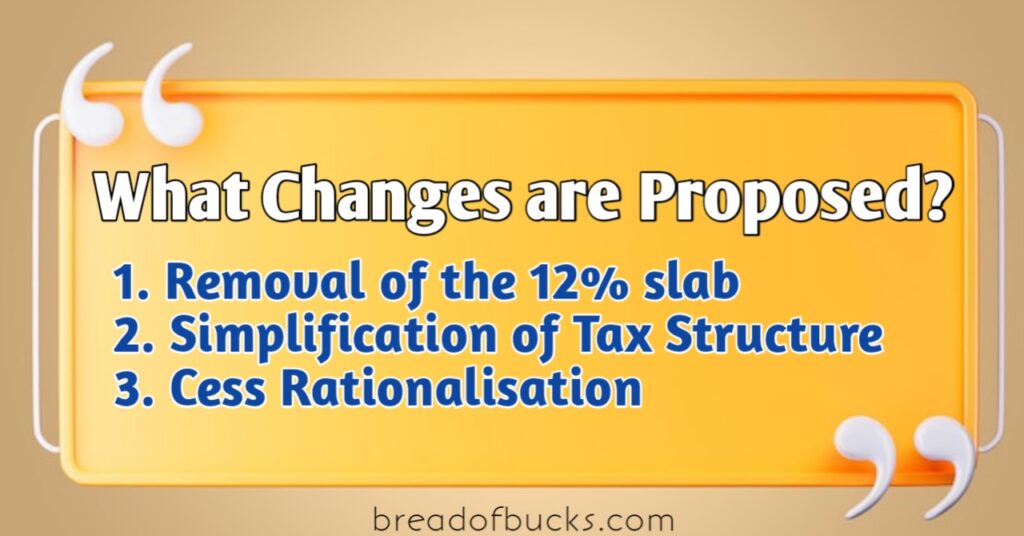

What Changes are Proposed?

- Removal of the 12% GST Slab

- Items currently taxed at 12% could be:

- Moved down to 5% (for essential or mass-consumption items)

- Or moved up to 18% (for relatively higher-end consumption items)

II. Simplification of Tax Structure

- Instead of five major tax slabs, India may move to a three-slab structure:

- 5%, 18%, and 28% (with 0% for essentials continuing)

- Special rates (0.25% and 3%) may remain untouched

III. Cess Rationalization

- The cess used to repay

- The 2.7 lakh crore debt taken auring the pandemic is being repaid from cess collections valid until March 31, 2026.

Point to be Noted

- The 5% slab covers about 21% of goods

- 12% slab covers 19% and •18% slab includes nearly 44% of goods.

- Only 3% of items fall under the highest 28% slab.

Why is our focus on the 12% slab?

- The 12% slab has overlapping items that are hard to categorize.

- Removing it allows a cleaner split between merit goods and non-merit goods.

- It is politically and economically easier to distribute 12% items than to collapse the 5% or 18% slabs, which affect either the poor or government revenue significantly.

Purpose of the Reform

- Simplify compliance – Businesses currently face challenges managing multiple slab rates; fewer slabs means less confusion.

- Reduce litigation – Fewer disputes about classification of goods between slabs.

- Prepare for Free Trade Agreements (FTAs) – A cleaner tax structure boosts India’s image for international trade negotiations.

- Boosts Ease of Doing Business – Helps MSMEs, exporters, and investors with predictability in tax burdens.

Which Good Shifting in Which Slab

Goods May Shifting to 5%slab :

- Ghee, butter

- Processed foods like •snacks

- Fruit juices

- Some mobile phone components

- Umbrellas

Goods May Shifting to 18%slab :

- Mobile phones (already partially at 18%)

- Ready-made garments above ₹1,000

- Household electronics

- Fertilizers (though politically sensitive)

Impacts after this major change

For Consumers (Mixed effects):

- Some goods will become cheaper (if moved to 5%)

- Some goods will become more expensive (if moved to 18%)

For Businesses :

- Simpler input tax credit claims

- Fewer classification disputes

- MSMEs may face less confusion on product pricing

For Government & States:

- Might lead to initial revenue volatility

- But long-term increase in tax compliance and transparency

- State governments are being consulted to ensure compensation adjustments if revenue dips

Challenges may be have

- States’ reluctance: If many items go to 5%, states may fear revenue loss.

- Inflationary risk: Moving some 12% items to 18% could spike retail prices temporarily.

- Political pushback: States going to polls may resist tax hikes on sensitive goods.

Timeline

- July 2025: PMO gives green signal for overhaul.

- August 2025: Expected GST Council meeting to present full proposal (after the monsoon session of Parliament).

- Implementation timeline: Possibly FY 2026 onwards (April 2026), subject to state consensus.

For more information follow us :- click here