Insurance – Smart Protection for Life & Assets

Life is full of risk, and humans naturally try to reduce them. Insurance is an age-old method of risk sharing and economic cooperation. It is a social device where many people share the losses of a few. Insurance helps manage big, uncertain, and changing Liabilities by collecting small fixed payments (premiums) from many to cover large losses for a few. It provides financial protection against risks like fire, sea damage, accidents, or death. Though it can’t prevent risks, it helps reduce the financial impact.

What is Insurance?

Insurance is a financial arrangement where you pay a premium to an insurance company in exchange for protection against potential financial losses. It helps cover risks like accidents, illness, damage, or death, offering financial security and peace of mind.

Why Insurance?

- Life is full of risks

- Humans try to avoid or reduce risks

- Insurance is a social and economic tool to manage risks

Purpose of insurance

- Protects against financial loss (fire, sea damage, accidents, death, etc.)

- Cannot prevent risk but reduces the impact

- Encourages savings and investment by securing the future.

Main aspects of insurance:

- An asset : The item or life being insured.

- The risk insured against : The event causing loss (e.g. fire, accident.)

- The principle of poling : Many people contribute to a common fund.

- The contract: – Legal agreement between insurer an insured.

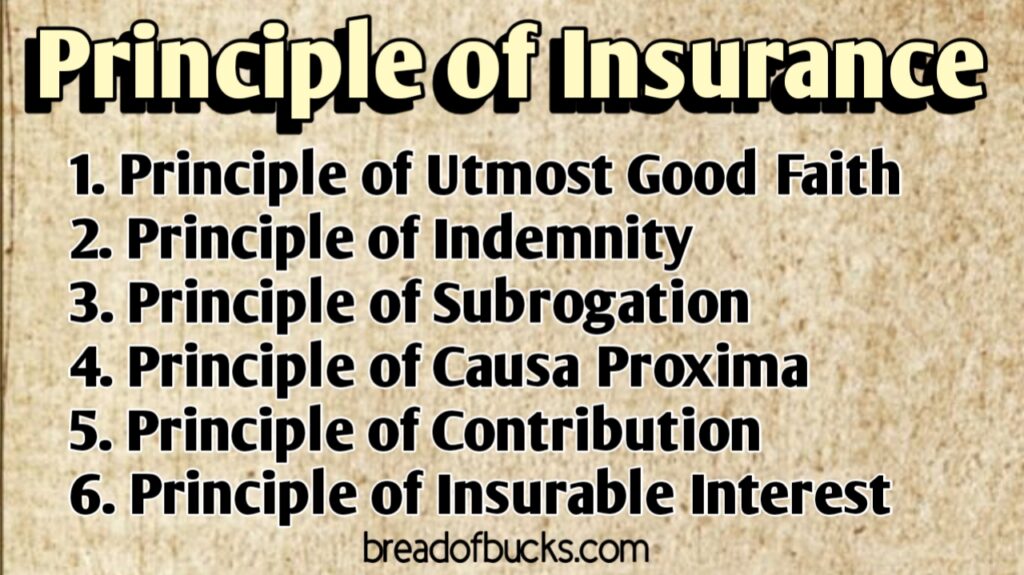

Principle of insurance

An insurance contract is based on some important rules. These rules help build trust between the company and the customer.

1. Principle of Utmost Good Faith

Both you (the insured) and the insurance company (the insurer) must be honest and open.

You must tell all the important facts clearly — no hiding, no lying!

If you hide something important or give wrong information, the contract can be cancelled.

Example : If you’re buying health insurance, and you hide that you have diabetes — the company can cancel your policy when they find out!

Remember : Even if you hide something by mistake, and it affects the company’s decision, it can still make your policy invalid.

2. Principle of Indemnity

You should not make profit from insurance — just recover your actual loss.

If something is damaged or lost, the company will pay only the real value of the loss, not more.

Example : If your car is damaged and the loss is ₹50,000, you’ll get only ₹50,000 — not more.

3. Principle of Subrogation

After you receive your claim from the insurance company, your right to sue the person who caused the damage passes to the insurance company.

Example : If someone hits your car and you get the claim, the insurance company can now recover the money from the person who caused the accident.

4. Principle of Causa Proxima

Insurance covers the closest and direct reason of the loss — not something that happened long ago.

Example : If your goods were damaged due to heavy rain (not some old leak), then the nearest cause (rain) will be considered.

5. Principle of Contribution

If you have multiple insurance policies for the same thing, you can’t claim full amount from all. All companies will share the loss in proportion.

Example : If you insure your house with 2 companies and loss is ₹1 lakh, both companies will pay part of it, not full.

6. Principle of Insurable Interest

You must have a legal or financial interest in the thing or person you’re insuring.

Example : You can insure your own house or car, but not your neighbor’s – because you don’t have a financial loss if something happens to theirs.

Final Thoughts

Understanding these principles helps you make better decisions when buying insurance and ensures you’re treated fairly when you make a claim.

So next time you pick an insurance policy, remember: it’s not just about premiums it’s about trust, honesty, and fairness!

For more Information follow us :- click here